Intellectual Property Rights

One of the most attractive frameworks for Intellectual Property Rights management in Europe

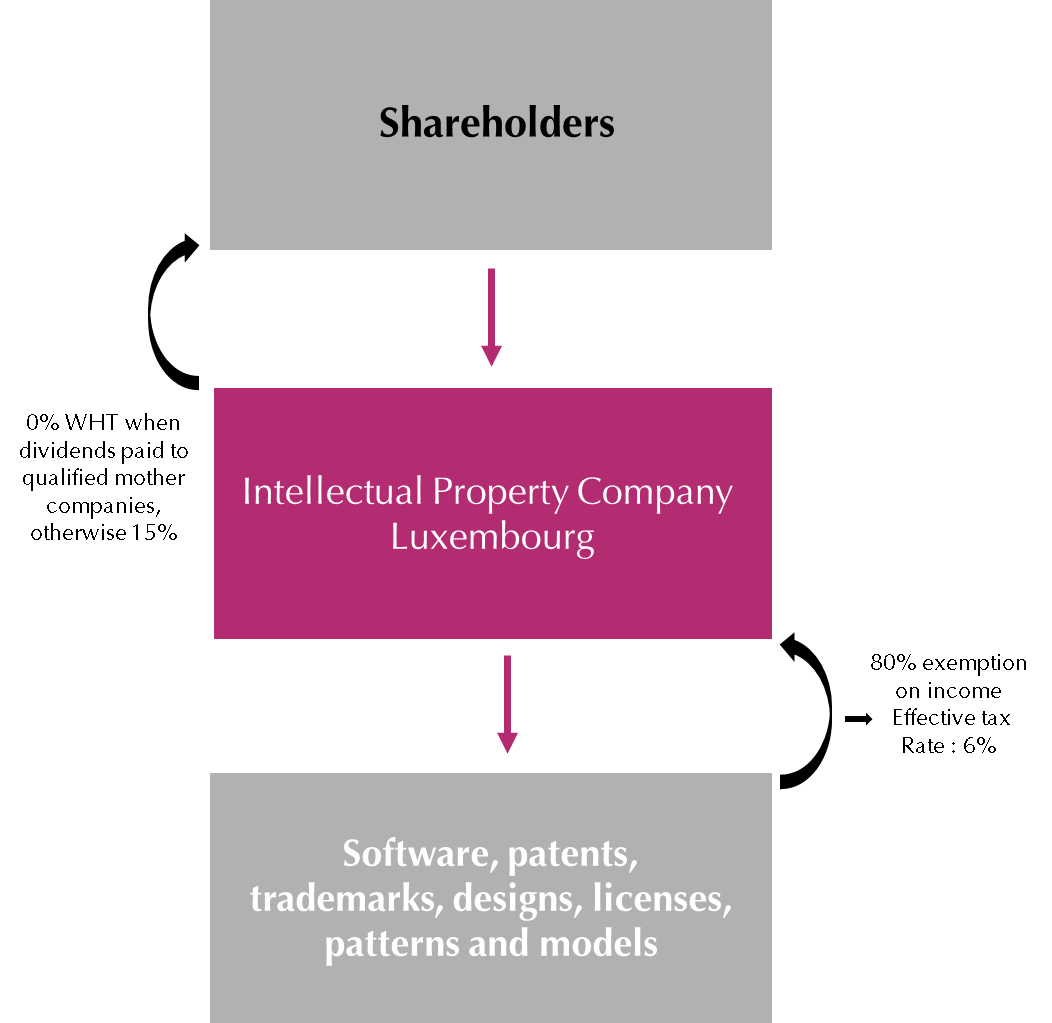

The Luxembourg tax regime aims at encouraging Intellectual Property (IP) companies to invest in intellectual property and research and development (R&D) through an effective tax rate on IP income of around 5%.

Description

One of the most attractive frameworks for Intellectual Property Rights management in Europe

The Luxembourg tax regime aims at encouraging Intellectual Property (IP) companies to invest in intellectual property and research and development (R&D) through an effective tax rate on IP income of around 5%. The attractive IP tax regime available for a Luxembourg IP companies is now applicable to following IP rights:

- patents

- trademarks

- models

- design

- authors’ copyright related to software

- and some other IP

These assets should have been acquired or created after 31 December 2007. There is no minimum holding period.

The Intellectual Property Right tax regime : (Article 50bis and 50ter Luxembourg Tax Code)

- Exemption of 80% of the net profit derived from the royalties received by the Luxembourg IP company on its IP rights;

- Exemption of 80% of the net capital gain realised upon disposal of these IP rights by the Luxembourg IP company;

- 100% exemption from wealth tax on the IP rights value held by the Luxembourg IP company;

- If the Luxembourg IP company has developed the IP rights itself, then it allows a deduction equal to 80% of a deemed income of the IP Rights used by the Luxembourg IP company.

The Luxembourg IP company

The IP company can be set up in any form existing under Luxembourg company law. Investors, promoters, authors and IP developers often choose the S.à r.l or the S.A. (with a minimum capital of 12.000 or 30.000 Euro).

The IP rights may be purchased or acquired by a contribution in kind from the company’s shareholder.

There is no restriction on the nationality, residence or domicile status of the shareholder in a Luxembourg IP company. They may be a corporate or private individual.

Incentives offered by Luxembourg as one of the most attractive frameworks for R&D in Europe

As well as the specific IP tax exemptions noted above, Luxembourg IP companies, private research SPVs, R&D companies, and Funds, etc., also benefit from a range of incentives including R&D project funding of 25% to 100% (generally being subsidies or interest-rate subsidies).

Luxembourg is therefore ideally located in the heart of Europe for the incorporation of Intellectual Property Rights’ companies.

A new IP regime to comply with the Nexus Approach is available in Luxembourg

The Article 50ter allows a taxpayer to benefit from an IP regime (exemption at 80pc of income derived from IP) to the extent that the taxpayer itself incurred qualifying research and development (“R&D”) expenditures that gave rise to the IP income.

This is inline with the “OECD”’s document released on 6 February 2015 “Action 5: agreement on Modified Nexus Approach for IP Regimes”.

Gearup Solutions , for trust, communication and confidence

Gearup Solutions can provide you with guidance and knowledge to help you take full advantage of the favourable legal, taxation and regulatory frameworks available in the Grand Duchy.

Our specialists draw on in-depth, in-house knowhow to help you ensure that your intellectual property, and all circumstances, are fully considered and thereby structured to your best advantage.

Gearup Solutions will help to identify the key IP issues in your business, company or group; provide guidance on appropriate legal and tax structuring; inform you of all relevant licensing, cost-sharing and research and development variables; while also providing tried and tested advice on IP flows, financing, transfer pricing, and more.

In addition to offering advisory services, Gearup Solutions provides corporate services for clients; from the creation of an IP company, fund or start-up established in Luxembourg to the administration and management of the structure.